Are small-mid caps overvalued?

At the end of September 2020, The Australian Small Ordinaries Index (XSO) is 95% of the level it achieved at the end of 2019 and 89% of the peak achieved in mid-February 2020. The valuation of the XSO index, as measured by a 2 year forecast PE ratio is also back to around 95% of the level achieved in February 2020. In February 2020 COVID-19 restrictions, business uncertainty and significantly elevated global debt levels were not the issues they arguably are now. So are

Australian small-mid caps overvalued? Does this mean that equities in general and small-mid caps should be avoided?

Interest rates keep going down

Declining interest rates over a long period have undoubtably boosted underlying equity valuations. The US 10 year bond now yields around 0.65% compared with a low of 2.1% during the Global Financial Crisis (in late 2008) and 5.8% exactly 20 years ago. I started work in late 1989 when the US 10 year bond was yielding around 8%. A downturn followed and yields fell to 5.25% in late 1993 only to rebound to over 8% in late 1994. By comparison, the Australian 10 year bond from late 1989 to now has gone from yielding 14% to 0.8%. This now all seems like a bygone era.

The issue now is what may break this trend of ever lower interest rates? Will it be the fear of inflation that just doesn’t want to reappear or sudden concern about elevated debt levels everywhere? Will it be social developments and tension between the asset owning Baby Boomers and the young generations faced with high education costs and a housing market that seems beyond reach? Could it be the impact of global trade going backward as a result of current tensions?

TINA and FOMO

TINA (There is no Alternative – to equities) and FOMO (Fear of Missing Out) have combined to create a rapid rebound in equities. This is evident in the volume records being set on many world equities exchanges and significantly increased participation by retail investors. In 2H FY20 the ASX reported a 52% increase in cash equities volumes over 2H FY19. The ASX also noted 7 million trades in one day in March 2020 which was +122% vs the pre COVID-19 daily record set on the 6 August 2019^.

We are currently in a recession. However, the equity market has been moving in the opposite direction vs struggling underlying economies. There are two principal views among investors, in our opinion, on what is wrong or not. Traditional investors are concerned about the impact of recession, debt levels and general economic risk. Traditional investors are also likely to have more than half an eye on wealth preservation. The second, newer group, perhaps more prevalent in the additional volume being generated across world stock markets, are likely to be younger wealth seekers who don’t want to miss out this time the way they have in housing and equity markets for what seems like forever.

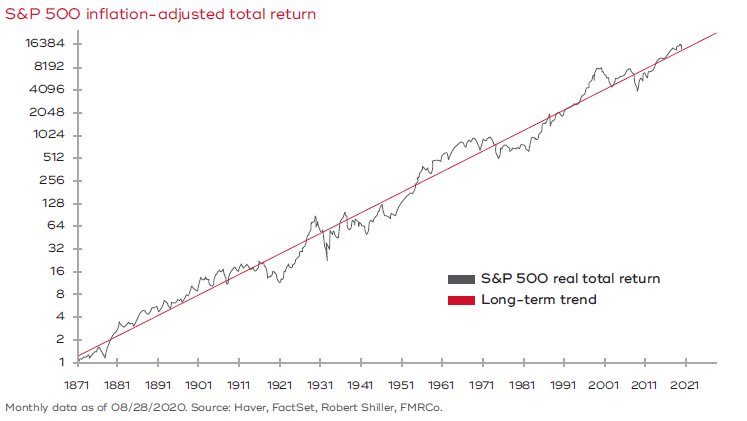

The long term

Let’s reflect on the following very long-term chart of equity markets.

If you take a longer perspective the adage of “it’s not timing the market that matters its time in the market” that counts.

Zero % interest in the bank doesn’t work but over a longer perspective the equity market is still very likely to rise. A long run return above zero is still better than zero.

It appears to us that taking a longer-term perspective reconciles the concerns of both groups of investors and that both may therefore be right. A longer-term perspective reduces the prospect of wealth destruction for the first group and for the second group anything better than zero will create some wealth. A bank at-call deposit will now produce virtually none. Even a 1-year term deposit will yield less than 1% compared with an equity market that offers 3 day settlement. However, a 10 year investment in equities seems likely to do considerably better than either.

Australian and US interest rates at current levels are significantly lower than they were at the start of 2020. The US 10 year bond has declined from around 1.9% to 0.65% since December 2019. Interest rates also seem unlikely to rise rapidly given the levels of debt now outstanding. In this context the 2 year forecast PE for the XSO index, currently sitting at around 18.5x and like the start of this year, does not seem excessive. We believe that within the small-mid cap space it is always possible to find growth being driven by innovative management and often global opportunities. In addition, COVID-19 has produced structural change opportunities that have accelerated. The very long-term chart of the S&P 500 above highlights that if you can invest in compounding growth you ultimately will get paid. In that context we believe that don’t need to fall back on TINA and FOMO to justify the current valuation of Australian small-mid caps. You do however need to take a longer-term perspective.

Author: Stephen Wood, Principal and Portfolio Manager

^ (Source: ASX FY20 Annual release presentation 20/8/20).

Disclaimer

This material has been prepared by Eiger Capital Pty Ltd ABN 72 631 838 607 AFSL 516 751 (Eiger). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable, but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed.