Increased Market Volatility – A 2025 Update

In early 2024 we wrote a note attempting to quantify the perception that volatility around results during the February 2024 interim results season had increased materially.

The Vibe

The AFR wrote an opinion piece on March 3, 2024, noting that the corporate reporting season was not the sleepy affair it once was. They noted, using the 20% positive and negative share price reaction of Reece and Corporate Travel respectively as examples, that the days of subtly guiding the market to a safe low volatility consensus appear to be over.

The AFR noted that in their opinion that Reece tended to be less willing to constantly update the market while Corporate Travel was more inclined to provide incremental updates between formal semi-annual reporting dates. They then noted that neither approach seemed to have, in this instance, achieved the lower volatility outcome perhaps desired by the requirement for continuous disclosure. The ongoing refinement of Factset, Bloomberg or Visible Alpha consensus data, that is available to anybody who is prepared to pay for it should you would think, other things being equal, also make it easier to minimise result day volatility.

REH, CTD ASX: Corporate Travel and Reece trip up traders in wild reporting season (afr.com)1

The Australian also wrote an article on March 8 titled:

“What’s to blame for corporate shocks this reporting season”

Woolworths, Qantas, other corporate shocks the result of poor communication | The Australian2

As a small and mid-cap manager we are not as familiar with the ASX top 50 stocks mentioned in this article other than to note that we believe that ASX 50 stocks tend to be less volatile than small and mid-caps. This article refers to a 17% decline in the result day share price of Lend Lease which appears to us to be small cap like in its quantum.

Top-down numbers

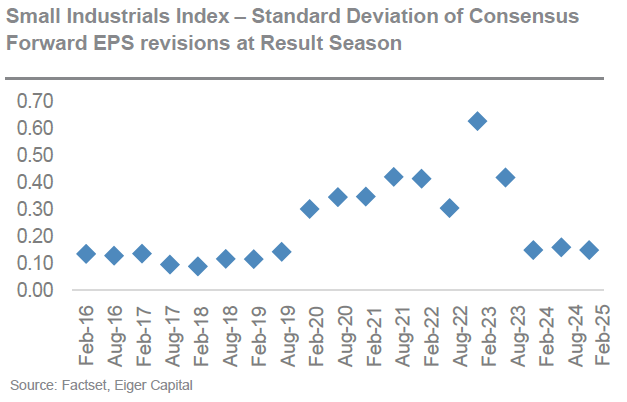

An analysis of the S&P ASX Small Industrials Index over the February 2024 reporting season indicates that the size of forecast EPS revisions has reverted to pre – COVID levels. Updating this chart confirms this conclusion. The August 2024 and February 2025 EPS revisions are low and in line with February 2024.

The standard deviation of EPS revisions in February 2024 was in line with the period from February 2016 to August 2019. By February 2020 COVID had already become widespread in China, Italy and Iran and was beginning to rapidly spread. From mid-February 2020 to the end of that month the ASX 200 fell just over 9% having risen slightly in the first half of that month. The reporting periods from August 2020 to August 2023 have seen elevated EPS revisions as economic activity was very unevenly distributed with some sectors being significant winners (e.g. home delivery and home furnishings) and some significant losers (e.g. travel). During the COVID reopening period from early to mid-2022 there have still been significant variations in earnings outcomes as global supply chains have struggled to normalise and energy prices were disrupted by the start of the Russia- Ukraine war.

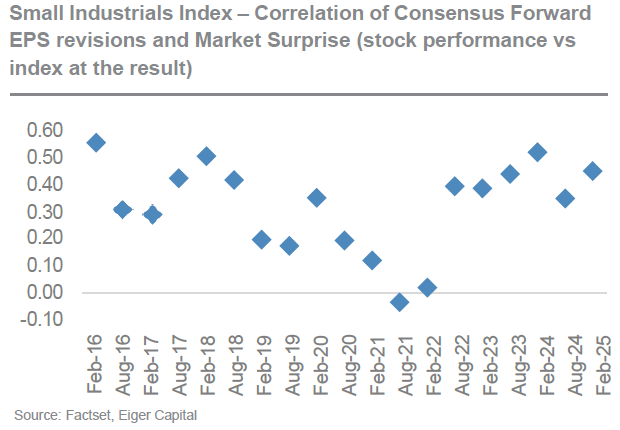

In addition to the variance of EPS revisions across the Small Industrials index declining in February 2024 the correlation of positive and negative revisions to the share price reaction increased back to the top end of the range witnessed prior to the onset of COVID. This is also confirmed by the addition of data from August 2024 and February 2025 data.

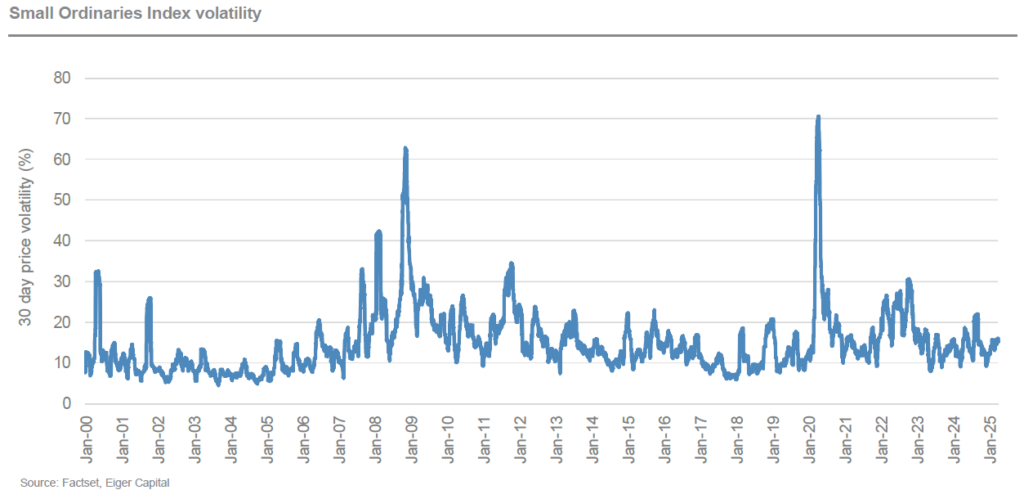

Finally at the Small Ordinaries index level volatility remains low and at pre-COVID levels. The following chart highlights that the two significant spikes in index volatility were in 2008-2009 (Global Financial Crisis) and 2020-2021 (COVID). This is also confirmed by updating this data to the February 2025.

Bottom-up Numbers

The updated analysis above suggests that the conclusion previously reached that the variability of earnings revisions has fallen. Share price reactions are at least in the expected direction given an upward or downward earnings revision and the overall volatility of the Small Ordinaries Index remains at low levels. Does it therefore follow that, as noted in the business press, that reporting seasons are now but a dull affair?

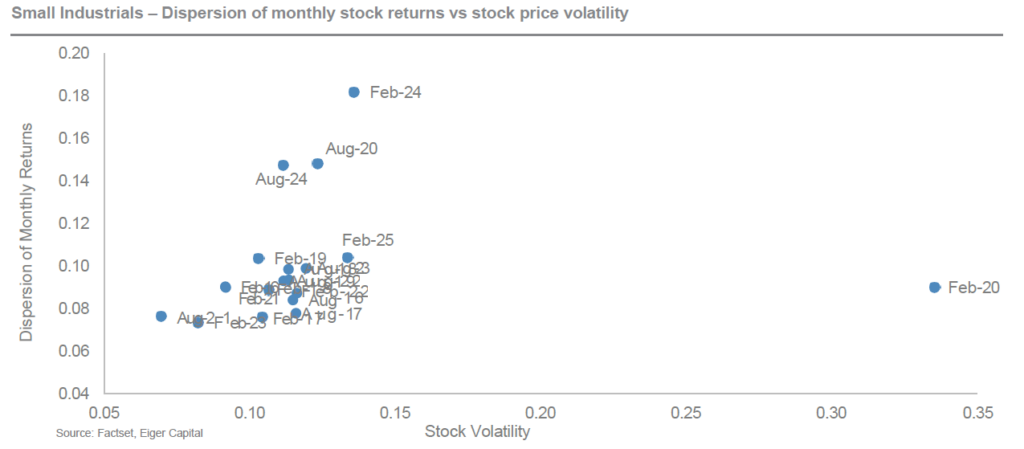

In attempting to look at this further we have compared the variability of monthly stock returns with the dispersion of the intra-month share price high and low. The x-axis takes the individual stock return over the relevant month and calculates their variability. So, for example the variability of stock price returns in February 2020 was extreme. There was a very large spread of high and low returns that month. By comparison the variability of returns in February 2024 was lower and more in line with the upper end of the normal range. The reporting period with the lowest variability of monthly reporting season returns in our analysis was August 2021.

So individual stock returns in the month of February 2024 were not outside historic ranges, However the story does not end there. The y-axis measure what happened within the month to individual stocks. This axis takes the intra-month high and low for an individual stock and measures the size of that dispersion. By contrast this was by far the highest recorded in our analysis. The evidence revealed by adding August 2024 and February 2025 is that overall stock return volatility has remained within a historic band (x-axis). The evidence around intra-month high and low share prices is less clear. The dispersion of high and low prices for individual stocks has remained above historic bands but the dispersion declined in August 2024 and again in February 2025. The outcome for February 2025 is still above the historic band but not significantly so.

A couple of anecdotes

While not the central thesis of this note, and perhaps delving into day-to-day stock movement, it seems interesting to highlight a couple of slightly absurd stock price movements during February to continue to highlight changes in market structure and behaviour. Audinate released its result on February 14 and the share price promptly increased 37% over the next few days. By March 7 the price was back to the mid-February starting point and by the end of March was 18% lower. So can we conclude that somebody (or something) decided the result was better than expected (hence the initial reaction and likely short covering) but that within a relative short period of time the reverse was likely. The result was in fact worse than expected hence the price fall of 40% from the peak. Our view is this is likely a combination of reduced liquidity and a series of decisions made by a something (not a someone). We would love a proponent of the efficient market hypothesis to explain this.

Shifting to a slightly bigger stock than Audinate (which at $10 has a market capitalisation of around $800m) to one of the stocks noted for volatility in February 2024, namely Corporate Travel. Corporate Travel announced their interim result on February 18 and promptly the share price increased by 18% by February 21. By the end of March, the share price was down to $13.91 or 8% below the pre result price and 22% below the peak also on February 21. There may have been other news over this time period, but you would think the dominant news would have been the result. You would think it was either A: Better than expected or B: worse than expected. It turns out that as with Audinate there are decisions being made by somebody or something that mean that neither is the correct answer. The correct answer is C: it was both better and worse than expected. Go figure.

Liquidity?

In April 2025 as in April 2024 we have a view that there could be an overall decline in continuous disclosure. This is despite a steady increase in consensus data availability and a steady increase in the level of detail notably by the widespread use of Visible Alpha in the Australian market. This is backed up by noting that the size of EPS revisions and their immediate impact on share price reactions appears to have returned to pre COVID levels. Overall index volatility remains within normal levels and certainly nowhere near GFC or COVID levels.

Overall monthly return volatility is also normal but intra-month volatility increased materially in February 2024 and has declined to still elevated levels over the subsequent levels.

The following chart highlights the rolling 12-month liquidity of the small ordinaries index. Once again, we can see the significant spikes caused by COVID as portfolios were repositioned at the start and toward the end of the pandemic.

What appears to be the case though is that the velocity of turnover relative to the size of the index is at or close to historic low levels.

What could be the causes of this? One possible explanation is the lack of IPOs in the last few years. There is little doubt IPO’s increase overall liquidity for a short period of time but in our experience, this normalises within a week at most. Takeover activity similarly briefly increases liquidity significantly on the day a bid is announced. There can also be significant periods of liquidity in a takeover as shares swap hands between long term investors and shorter-term takeover specialists as a takeover is finalised. The downside of a takeover is that ultimately it may reduce the size of an index leading to less opportunities for long term investors.

We believe a factor worth considering is the impact of passive and near passive investment management. Global ETF’s and index funds, that trade based on their own flows and not necessarily daily fundamental news flows, appear to own around 20% based on the information available in Factset. In addition to this investment, we believe there would be additional difficuly to quantify holdings by wholesale passive funds who manage money on behalf of institutional holders either internally or externally. There are also strategic holdings in some companies, notably those that are very long duration and infrastructure like that do not participate in market liquidity.

Using the chart below the velocity of trading, if we exclude the COVID period, has fallen from around 70% to 56% at present. We do not think that it is implausible that the bulk of this decline is the accumulation of passive and near passive investment styles. This factor is likely to have impacted large cap indices earlier than small cap benchmarks as constantly rebalancing passive funds ironically is easier in more liquidity.

In addition to reduced liquidity, that could be due to increased passive or other factors, we would note that we witness daily the impact of systematic investment managers. A systematic manager has a set style, often enhanced by algorithms that will trade with minimal human intervention. This style, well run forms a part of the broad church of management styles that make up a market.

Explaining the Vibe

We believe that what the business reporters are witnessing isn’t a breakdown in continuous disclosure but rather increased share price reactions to news based on the evolution of investment styles. Liquidity is currently at a low level and concurrently we believe that execution of large orders by systematic investors has become more aggressive.

Will liquidity continue to structurally decline, and will short term volatility continue to increase? We aren’t sure but either way it doesn’t concern us as we plan to maintain a level of funds under management that will allow us the flexibility to execute our investment style. To some degree it may provide additional opportunities particularly if stocks continue to move aggressively and then rebound intra month.

Author: Stephen Wood, Principal and Portfolio Manager

1. “Corporate Travel and Reece trip up traders in wild reporting season”, Australian Financial Review, 3 March 2024. May require paid access to view full article. 2.”What’s to blame for corporate shocks this reporting season”, The Australian, 8 March 2024. May require paid access to view full article.

This material has been prepared by Eiger Capital Limited ABN 72 631 838 607 AFSL 516 751 (Eiger Capital). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed.![]() formal semi-annual reporting dates. They then noted that neither approach seemed to have, in this instance, achieved the lower volatility outcome perhaps desired by the requirement for continuous disclosure. The ongoing refinement of Factset, Bloomberg or Visible Alpha consensus data, that is available to anybody who is prepared to pay for it should you would think, other things being equal, also make it easier to minimise result day volatility.

formal semi-annual reporting dates. They then noted that neither approach seemed to have, in this instance, achieved the lower volatility outcome perhaps desired by the requirement for continuous disclosure. The ongoing refinement of Factset, Bloomberg or Visible Alpha consensus data, that is available to anybody who is prepared to pay for it should you would think, other things being equal, also make it easier to minimise result day volatility.