Structural tailwinds for 2020 and beyond

At Eiger Capital, we’ve always liked to invest with the aid of a good old-fashioned tailwind. In our humble opinion, tailwinds don’t come much better than the global shift to renewables in energy generation and the associated electrification of almost all forms of transport.

And whilst 2020 may turn out to be too soon to put this theme into the “can’t ignore in 2020” bucket, investors with the capacity for more than a twelve-month investment horizon can’t and shouldn’t ignore this theme.

We like structural change as a precipitator of investment opportunity. In Aussie small cap equities, structural change can be found impacting many companies and industry sectors. Transport electrification and lithium battery-based energy storage is delivering significant structural change to the transport and energy utility sectors, amongst others.

It’s often more difficult to pick the timing of such change than its direction and ultimate destination. Nevertheless, history teaches us that sometimes a significant change can happen much faster than anyone expects. Mass adoption of electric vehicles and rising levels of renewable energy generation may indeed surprise many over the next five+ years.

Theme 1: Transport electrification

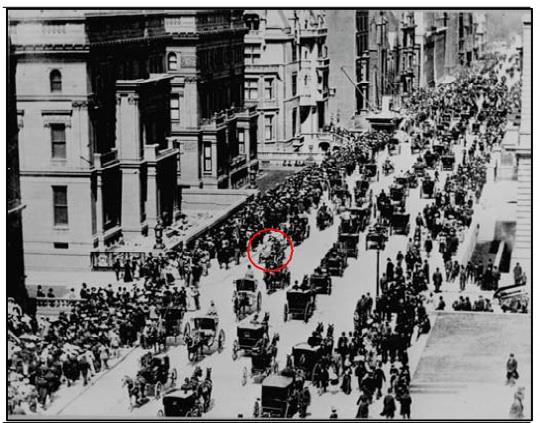

Take the example of the last major structural shift in transportation technology just over 100 years ago. We do like to use these two photos because as they say, a picture (or two) tells a thousand words. Who would have thought that back in the year 1900 as one sat watching the Easter parade on 5th Ave, New York City that the one curiosity on parade, the single motor car amongst all the horse and carriages, would come to dominate the same parade just under a decade and a half later?

Over this relatively short time frame, all but one of the horse and carriages had disappeared from the parade. It was now dominated by internal combustion engine (ICE) based motorised transport.

NYC Easter Parade: 1900 vs 1913

Easter Parade 1900: 5th Ave, New York City

One automobile

Easter Parade 1913: 5th Ave, New York City

One horse and carriage

Source: US National Archives

Even today if one is prepared to look, there is already significant evidence of the way the future may look like in as little as 5-10 years’ time. Tesla has no doubt copped a lot of justified criticism for its struggles to produce its innovative electric vehicles in sufficient economic volumes. However, there is little doubt that there is strong and growing demand for their products. The number of Model 3’s starting to appear on our local streets in recent months shows Australians are indeed embracing this change.

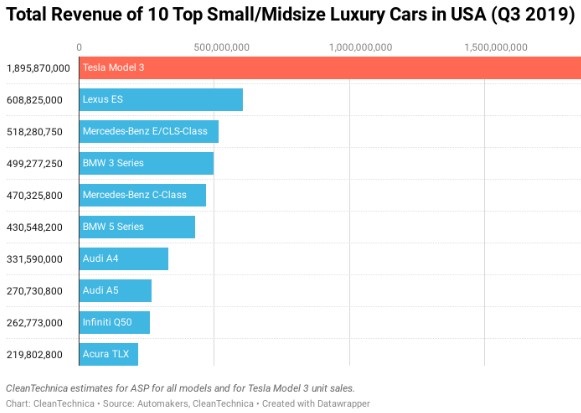

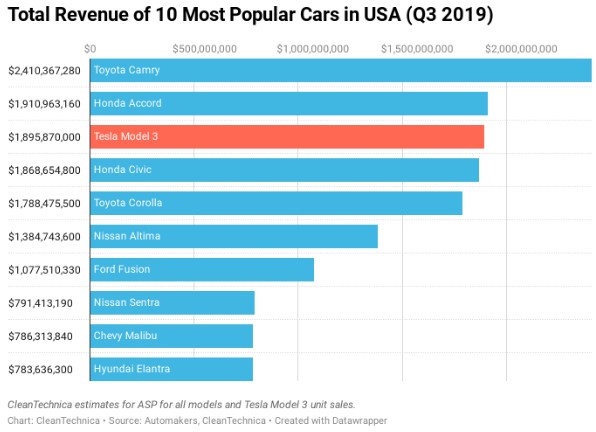

But it’s not just trending in Australia. The Model 3 is the largest selling luxury small-medium car in the US on a sales revenue basis, by a long way. In fact, Model 3 sales revenue is greater than that of the numbers 2-4 combined. Even amongst all cars in the US the model 3 has the third highest sales revenue across all cars sold in the US in the September 2019 quarter. This ranking excludes pickup trucks because, just like in Australia, utes/pickups outsell cars in the US but nevertheless a good early indicator of likely future demand for EVs.

We believe demand for EVs could grow exponentially over the next 3-5 years as fruits of the US$60-100b being spent on R&D over the next decade by the large global auto companies appear in the form of many new EV models for consumers to choose from.

The trend to electrification won’t just end with cars

This year the NSW government announced a plans to replace all 8,000 or so diesel and gas buses in NSW with electric buses. Europe and China are already well ahead of Australia in this regard with many Chinese cities having fully converted to electric public transport fleets.

Even air transport will gradually move to electric, especially in short-haul routes. These routes are better suited to the limited range of battery powered planes. Short-haul routes require smaller more efficient planes with typically less than 1000kms of range. At a lower cost point, many thin and currently uneconomic regional air routes could be made viable. Small electric commuter aircraft such as the Eviation “Alice” provide airlines with a lower unit cost allowing them to offer greater frequency and lower pricing.

This aircraft, for example, has capacity for nine paying passengers and costs US$200 per flight hour to run. This compares to about US$1,000 per flight hour for an equivalent turboprop, as typically used on regional routes in Australia. With aircraft such as these, the economics of regional commercial air routes are materially improved. This could open a new large and unaddressed segment of the market.

Theme 2: Renewables

We haven’t even scratched the surface of the full opportunity for lithium battery technology in years ahead. For example, there is rapidly rising demand for batteries as energy storage solutions, not just in homes but at grid scale. We have witnessed a significant increase in the number of recent announcements on planned new large-scale battery storage projects, especially as the share of renewable fed into our power grid rises. Large batteries are very effective at not only storing excess energy generated at peak renewable periods but also at moderating the large frequency fluctuations impacting the grid from renewables sourced power generation. The fact is that wind and solar are now the lowest cost source of incremental new generation and getting cheaper still. Solutions to the unique challenges arising from higher levels of renewables must be found and lithium batteries are a key part of that solution.

So, what does this all mean for investors in 2020 and beyond?

Firstly, we think investors looking to capitalise on these structural tailwinds need to have more than a one-year investment horizon. As the old investment saying goes, many overestimate what can be achieved in one year and underestimate what can be achieved in five years. If investors do indeed have more than a one-year horizon (as we ourselves take when investing), then there may be some attractive investment opportunities in some Aussie small caps.

For those with a longer investment horizon and higher risk tolerance, Pilbara Minerals (ASX: PLS) appears well placed to capitalise on the rising long-term demand for lithium batteries. Its stage 1 lithium spodumene mine is complete and ramping up well although better recoveries are the last challenge still facing stage 1 (expect evidence of better recoveries by the end of calendar 2019). It has a very large resource with significant proven reserves and opportunity to increase this further with more exploration. The mine should sit in the bottom quartile of the global cost curve when fully scaled up and further vertically integrated with downstream lithium hydroxide conversion capacity. It has brought strong and credible industry equity partners onto its register and has long term plans to more than triple current production as demand builds. The share price is presently being impacted by the short-term oversupply of lithium inputs into the global battery sector but this should reverse over the next 1-3 years, especially with the rising number of recent capacity deferrals by competitors (e.g. Mineral Resources placing their Wodgina mine on care and maintenance/Tanqui deferring their lithium hydroxide expansion plans in WA).

Another strong but lower risk beneficiary of the transport electrification and renewables themes is Lynas Corp (ASX: LYC). It is the only non-Chinese scale supplier of some critical rare earth elements used in many high technology sectors. The Neodymium (Nd) and Praseodymium (Pr) it produces (as NdPr oxide) are key ingredients in the manufacture of permanent magnet-based electric motors. These are critical parts of both electric vehicles and wind turbines. They are also extensively used in many defence industry applications and cannot be sourced from elsewhere globally except Lynas Corp (20% global share) and Chinese sourced supply (80% global share). Current western tensions with China on various fronts make this supply source problematic for western customers in the long term.

Lynas has spent the past seven or so years building and fine tuning their large Malaysian production facility and developing their high grade and large reserve mine in WA. These assets are globally unique and valuable. They are not easily replicated, even with limitless funding, due to the special production IP internally built up in their Malaysian plant. The business is very well managed, post capex and is cashflow positive. It is also very leveraged to growing demand for EVs, renewable wind energy and other new high technology themes.

As a demand reality check for Pilbara and Lynas:

- each Tesla Model 3 produced needs about 1kg of NdPr oxide and about 60kg of lithium hydroxide (or about 420kg of 6% spodumene)

- each 1Mw of wind turbine capacity need about 200kg of NdPr oxide

Disclosure – The Eiger Australian Small Companies Fund has positions in both Pilbara Minerals and Lynas Corp.

Author: Victor Gomes, Principal and Portfolio Manager

The information in this article is current as at the date of publication and is provided by Eiger Capital ABN 72 631 838 607 AFSL 516 751. It is intended to be general information only and not financial product advice and has been prepared without taking into account your objectives, financial situation or needs. Past performance is not a reliable indicator of future performance.